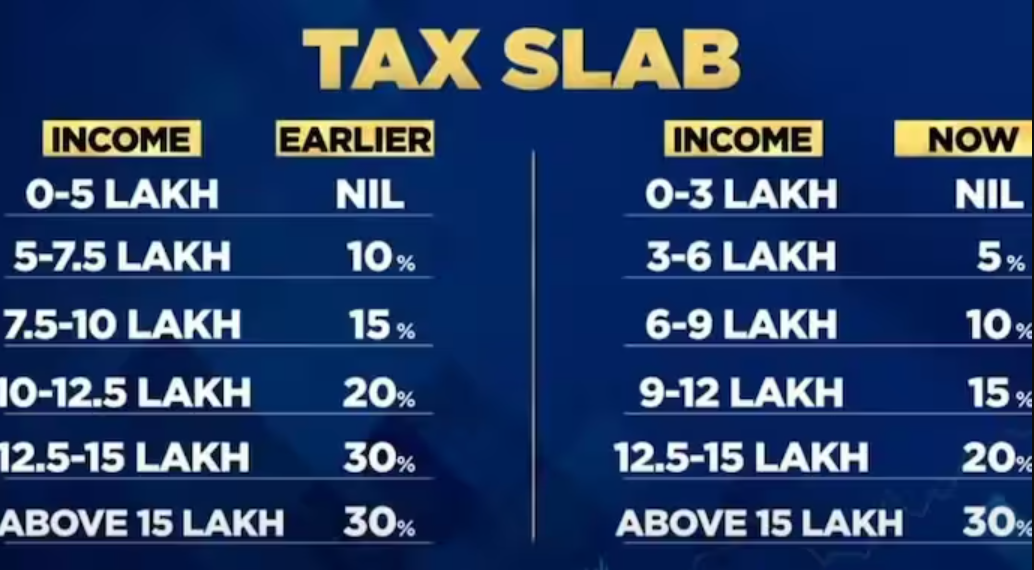

Choosing the new tax regime announced by the Indian government can be a daunting task for taxpayers. While the new regime offers lower tax rates, taxpayers must give up several deductions and exemptions they were previously entitled to. Understanding the deductions and exemptions available under the new tax regime is essential to make an informed decision.

Read on while knowing that a life insurance calculator is a simple and easy-to-use tool you may use online to determine the amount of coverage required based on your needs.

While the new tax regime offers a lower tax rate, taxpayers must assess their tax liability under the new and the old tax regimes before deciding. One of the main advantages of the old tax regime was the availability of various deductions and exemptions, which helped taxpayers offer life insurance tax benefits.

However, these deductions are not available under the new tax regime. For instance, deductions under Section 80C for long-term savings, Section 80D for health insurance policy premiums, and Section 24 for home loan interest are not available under the new tax regime.

The old tax regime offered a deduction of up to Rs 1.5 lakhs under Section 80C against the life insurance premium which is not available under the new tax regime either.

Taxpayers can still avail of some deductions under the new tax law. For example, the standard deduction of Rs. 50,000 is available to all salaried employees. Furthermore, taxpayers can claim a deduction of up to Rs. 50,000 for National Pension System (NPS) contributions over and above the limit of Rs. 1.5 lakh under Section 80C. Additionally, interest income from savings accounts up to Rs. 10,000 is exempt from tax.

For instance, taxpayers can avail of an interest deduction paid on housing loans taken for a property rented out under section 24(b) in the new tax scheme. Rent received from the property is deducted from the interest paid on the mortgage, which lowers the taxable income from the property. It is significant to highlight that under the new tax system, the interest paid on housing loans taken for a self-occupied house is not deductible.

Similarly, taxpayers can now deduct employer contributions made to their National Pension System (NPS) accounts under section 80CCD(2) of the Income Tax Act. This deduction is limited to the contribution made by the employer to NPS that is made for the employee’s benefit, up to 10 per cent of the employee’s salary (Basic + DA). Along with deductions for NPS payments under section 80CCD(2) and interest on leased property under section 24(b), the new tax system also offers exemptions for voluntary retirement, gratuities, and leave encashment.

While the deduction on the life insurance premium may not be available under the new regime, the tax exemption on the life cover amount under Section 10 (10D) is available for taxpayers under both regimes.

Under the new regime, which will take effect as the default regime in FY23-24, deductions under Chapter VIA of the Income Tax Act of 1961—including the deduction for gifts made to certain charitable institutions or trusts under Section 80G, the deduction for interest income earned on savings accounts up to Rs 10,000 under Section 80TTA/80TTB for senior citizens, and the deduction for interest paid on student loan principal under Section 80E—will not be allowed. Taxpayers under the new system are required to relinquish these deductions.

However, under the current system, the contribution made by a private sector employer to a Tier 1 NPS account is eligible for life insurance tax benefits up to 10% of the employee’s basic wage plus a dearness allowance in any given financial year under section 80CCD (2). Additionally, suppose a taxpayer chooses the new tax system. In that case, they cannot claim exemptions like the leave travel allowance, house rent allowance, children’s education allowance, professional tax deduction, mortgage interest deduction, and deductions on certain investments and insurance policies, among others. However, under the new tax system, interest paid on a mortgage taken for a rental property may also be deducted by section 24(b), he continued.

As the tax system is a crucial aspect of a country’s economy, the Indian government has introduced a new tax regime to make the taxation system simpler and more beneficial for taxpayers. However, taxpayers must evaluate their options before adopting the new tax regime. The new system offers lower tax rates, making it more beneficial for taxpayers with lower tax slabs. Still, taxpayers must also consider the deductions and exemptions they were previously entitled to under the old tax regime.

The deductions and exemptions available before may not apply under the new regime.

Leading off, remember that a life insurance calculator is a simple tool to check the amount of premium you would have to pay.

I got good info from your blog